In Energy Return on Investment, systems ecologist Charles A. S. Hall argues that to truly understand most investments, one must view them in terms of energy. This is perhaps most obvious when considering the physical survival of wild animals and human hunter-gatherers. In both these instances, the food obtained through foraging or hunting must yield more energy than was required to procure it, or starvation ensues. Another way of understanding this is by applying the concept of energy return on investment (EROI), also known as energy returned on energy invested (EROEI). As with the more familiar metric of return on investment (ROI), EROI is a ratio of profit to expenditure–in this case, energy profit to energy expenditure. It is calculated by dividing the energy output of a given activity by the energy that went into that activity. An EROI of 1:1 or greater is one that is at or above the break-even point, whereas an EROI of less than 1:1 fails to break even.

This principle extends beyond the individual sphere to encompass entire human societies. Like the lone animal or hunter-gatherer of the previous example, a civilization must maintain a positive energy balance to survive. Most ultimately fail to do so, as evidenced by the long line of failed past civilizations. Consider the ancient Easter Islanders, whose downfall was described so well in geographer Jared Diamond's 2005 book Collapse: How Societies Choose to Fail or Succeed. Diamond recounts how the Easter Islanders relied heavily on fish, and to catch the fish they needed wooden boats. They were depleting their wood supply faster than it could regenerate, and eventually their efforts to obtain more wood no longer yielded positive energy returns in the form of food. Now fast forward to our time and reflect on what's happened with the EROI of our primary energy source. The oil that powers modernity once came out of the ground easily, but it now requires herculean investments of both money and energy (think offshore drilling, hydraulic fracturing and horizontal drilling) to obtain.

The dwindling EROIs of fossil fuels is the most important energy-related issue that almost no one has heard of. Gas prices and heating bills tend to be readily understood because they directly affect people in a financial or physical way. But for the average person, a concept like EROI is an abstraction. This must change if we are to make wise decisions about our energy future. Weeding out the worthwhile energy sources from those that have negative to barely break-even returns (e.g., hydrogen fuel cells, corn-based ethanol) will require that we look at the EROI of every potential energy resource with a critical eye. It is toward this end that Hall has written this book.

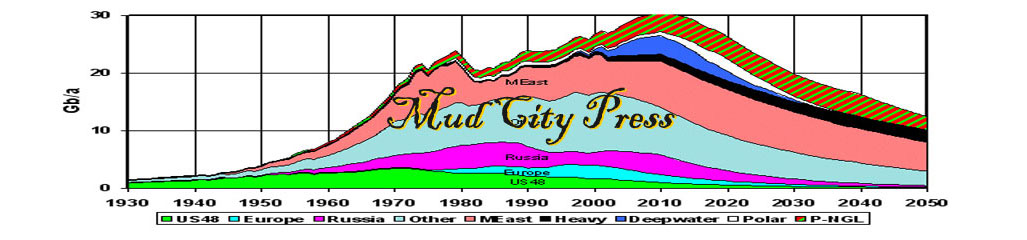

The nub of our situation, writes Hall, is that thus far we've operated according to the "best first" principle (to use a term coined by 19th century British economist David Ricardo) in our efforts to exploit energy. We've gone for the most concentrated and easily accessible resources first and left the less accessible ones for later. When we first began reaping the proverbial low-hanging fruit of American oil a century and a half ago, one had only to drill a hole in the ground in the right spot and oil would gush out from depths as shallow as several dozen feet. The EROI of U.S. oil was, at one point, as high as 100:1, and this terrific return goes a long way toward accounting for America's unrivaled military and industrial might at that time. Since then, American oil's EROI has deteriorated to a fraction of what it once was.

Given how little awareness there is about EROI, it's appropriate that Hall assumes no prior knowledge on his readers' part. His first few chapters go over the basics, including what energy is, how our understanding of it has developed, how fossil fuels formed and the limits imposed on both human and natural energy flows by the intractable laws of thermodynamics. The book's middle section examines energy in the contexts of biology and human economics. Its final stretch addresses the methodology of EROI analysis and rebuts criticisms that have been leveled against EROI.

The chapters on EROI and human economics cover a range of issues that Hall believes most economists need to better understand. Chief among these is the link between "secular stagnation" (economists' term for the anemia that has afflicted industrial economies in recent years) and the steady, ongoing decline in the energy density of fossil fuels. In Hall's view, this phenomenon is best understood in terms of what he calls the peak era model of economic growth. Since roughly 2005–the year in which production of conventional oil now appears to have peaked globally–oil prices have gyrated erratically and economic activity has shifted in lockstep with oil prices. We appear to be trapped in a cycle in which rising GDP stokes oil demand, which in turn spurs oil companies to pursue new resources. But because the remaining oil is increasingly challenging to access, prices skyrocket, which causes economies to stall, thus squelching the demand for oil. The resulting low prices lead to rising GDP and oil demand, prompting the cycle to begin anew.

For Hall, the answer to our predicament lies in a school of economic thought known as biophysical economics. Unlike conventional economics–which, due to its inordinate reliance on the social rather than natural sciences, violates basic laws of physics–biophysical economics emphasizes hard science-based evaluative measures. It is rooted in an awareness that nature is the necessary foundation for all human undertakings, and that energy derived from nature is what does the work of creating wealth.

If there's one thing that advocates of alternative (and supposedly climate friendlier) energy sources should take away from this book, it's the concept of embodied energy. Defined as the energy used to produce and deliver something, embodied energy is a factor that must be accounted for when analyzing the climate impact of any proposed energy source. While it's common for proponents of non-carbon-based energy resources to claim that they emit no carbon, this is true only if one ignores the fossil fuel it took to establish the initial infrastructure and keep it running. In the case of a nuclear power facility, for example, immense quantities of fossil fuel are required to mine, mill and enrich uranium, meaning that even though nuclear reactors release no carbon in their day-to-day operation, nuclear energy isn't carbon-free by any means.

Superb as this book is, it isn't faultless. Unfortunately, it required a more rigorous edit than it received. Grammatical errors appear throughout the text, and the last name of oil expert Kenneth Deffeyes is misspelled on every reference. Sadly, I fear that mistakes like these will dampen many readers' enthusiasm for the book.

But despite its editing issues, Energy Return on Investment is a solid introduction to a vital subject, and Hall is uniquely qualified to author it. Hall invented the very term energy return on investment, and he's done decades of seminal research on the phenomenon that it describes. As the current shale oil miracle goes the way of all mirages–causing the issue of energy depletion to reenter the public discourse in a big way–one can only hope that Hall's ideas will draw a great deal of well-deserved notice.